The Ultimate Guide to Understanding Credit Score

Your credit score or rating affects virtually every aspect of your financial life in ways you may even not know. With a good credit score, you can get lower rates for car loans, mortgages, credit card rates, and specific insurances.

Besides, it is used by some employer to gauge your credibility during hiring or promotion time. Therefore, it is safe to say that good credit can impact your career advancement.

Credit calculations can be confusing and complex to understand. The first thing to do to achieve an excellent credit score is to understand the ins and outs of your score.

In this guide, we will cover the basics of credit score- from what is considered a good credit score and composition of a credit report, to factors that affect it and how to improve your credit score.

Buckle up for a long read…

What Is a Credit Score?

This is 3-digit number summing all the details in your credit report. Many financial lenders use this score to determine your reliability in paying back loans, and whether or not you can meet your loan payment obligations. It is calculated based on the information in your credit report, such as your credit card balances and loan payment history.

There is a common misconception that each person has only one credit score that all lenders and credit bureaus refer too, but this is not true. There are multiple credit scores you are assigned to.

Why is this so? Because there are different approved scoring methodologies, different credit bureaus, and varying times in which your credit information is updated. Talking about bureaus, there are hundreds of scoring credit bureaus, but the most popular known ones are FICO Score and Vantage Score. Let’s discuss these two briefly.

What is a Good FICO Score?

Created by Fair Isaac Corporation, FICO scores are one of the most preferred types of credit scores by many lenders. They often range from 300-850. A score of 670 and above is considered a good credit score while those above 800 are termed to be exceptional.

What Is A Good VantageScore?

Developed by Experian, TransUnion, and Equifax, VantageScore uses a range of 300-850 as well. A score above 700 is considered good while above 750 is termed to be excellent.

Don’t worry about tracking all your credit scores. Instead, monitor those of well-known bureaus (FICO and Vantage) since they are the ones majority of lenders use to gauge your reliability in meeting your payment obligations.

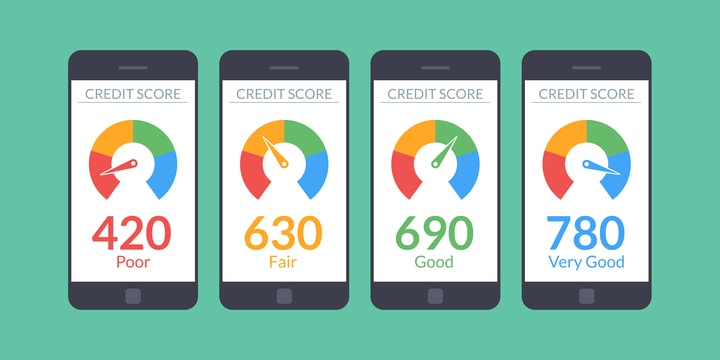

What Is a Good Credit Score? And What Is a Bad Credit Score?

As mentioned earlier, lenders and bureaus have their own scoring models that they use to determine your credit score for a particular service. Having a higher rating is not a guarantee that you will receive low-interest rates or be approved for credit. However, it can increase your chances of approval and getting better rates.

Based on FICO and Vantage range, scores of 781-850 are perceived to be ‘excellent’ which means that with this score, you can qualify for credit at lowest interest rates.

Scores of less than 601 are generally considered ‘unfavorable.’ This means you might not be accorded the best interest rates if you get loans, or you can be denied loans by many lenders.

To help understand more about these scores, let’s discuss the composition of your credit report.

About Credit Report

Credit reports comprise information that each credit bureau collects from different lenders. As mentioned above, there are hundreds of credit bureaus, and each produces consumer’s credit reports. However, the major bureaus that provide credit reports are Equifax, TransUnion, and Experian.

These reports are continually updated based on the actions you take and the information you give to financial institutions such as mortgage companies, credit card companies, banks, and online lenders.

Here are the three categories of the information entered in your credit report;

Credit history

This includes the number and type of active, closed, and opened accounts you have (auto loan, mortgage, credit card, etc.), credit utilization rate, age of credit accounts, your account balances, and your payment history, including instances of late payments.

Credit Inquiries

Whenever you apply for credit, and your lender ‘hard’ pulls your credit report, it reflects in your report as ‘hard’ or ‘soft’ inquiry. Only hard inquiries are public and affect your credit score for up to a year. It appears on your credit report for a period not exceeding two years.

Please note that;

Soft inquiry or ‘soft pull’ occurs when a lender or employers inquire about your credit report without your knowledge. Maybe when employers want to hire you, whereby they conduct a background check on you, or when a lender is sending you a credit card offer. It can also occur when you are checking your credit. This doesn’t hurt your score.

On the other hand, hard inquiry or ‘hard pull’ requires your consent. This is triggered when you apply for a mortgage, auto loan, credit card, student loan, business loan, or personal loan. It is recorded in your credit report, and thus, anyone who pulls our report will see the inquiry.

A hard inquiry takes out up to 5 points off your FICO score, but there are exceptions. Therefore, be careful with hard inquiries as they have an impact on your credit score.

Public records and collections

Information on your overdue debt from collection agencies such as suits, liens, foreclosures, and bankruptcies reflect on your credit report.

Your report also includes other details such as your address, date of birth, Social Security number, etc.

However, your salary, occupation, employment history, and your spending habits are not included in the credit report.

With that in mind, we can now discuss how calculations are conducted.

How is Credit Score Calculated?

Of course, your credit score is dependent on different factors, which we will discuss later on. For now, let’s discuss how the bureaus come up with the score.

FICO and other major credit bureaus such as Experian, TransUnion, and Equifax have their ‘secret’ internal algorithms of calculating credit scores.

One major factor they use to base these scores is your past and current financial actions as per the reports submitted by your current creditors. This information includes how long you have stayed with credit, the amount you owe creditors, and your payment tendencies. But as I said, the exact algorithm that these credit bureaus use remains a secret.

Your score changes based on the financial actions you take, and thus vary from time to time.

To give you a clearer picture of how the score is used, here is a summary of the process;

Your creditors send information about your past and current financial obligations to the credit bureaus who then use this information to calculate a score. This score is then made available to new creditors who use it to determine your reliability in paying future debts.

The higher your score, the more likely new creditors will approve loans and credit cards at lower rates.

Scoring agencies such as VantageScore and FICO place your score in the range of 300 to 850. Let’s discuss in details the factors believed to be in their ‘secret’ algorithm that determines where your credit score will rank.

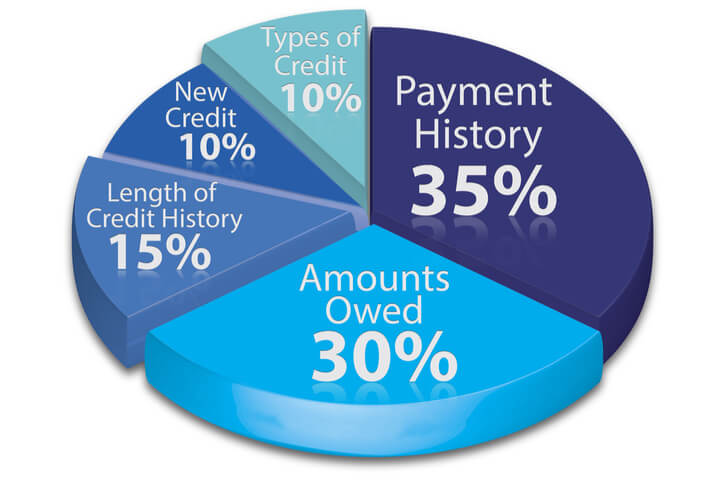

Factors That Impact Your Credit Score

Although there are different scoring models, the method of bettering your score is the same- paying your bills on time. Whether you are looking at VantageScore or FICO credit score, your credit score will be based on the information in your credit reports.

Here are the things that count when it comes to your credit score;

Payment history

This is one of the most important factors that influence your credit score. Having a long history of paying on time is healthy for your credit score while missing a payment could dent your score significantly. The impact is greater if your bill goes unpaid for a longer time. Therefore, a 30-day late payment will not be detrimental like a 60- or 90-day late payment.

Also, the amount you owe your creditor is also another factor. However, if you can start making payment and reduce the amount owed, then the impact will keep diminishing as well.

Credit usage

This is another important factor and one of the few that you may have full control on. The amount you owe to creditors such as auto loan, personal loan, student loan, or mortgage are all part of your credit usage equation. Your credit utilization rate is even more important.

Utilization rate is the ratio between total balances owed versus the total credit limit on all your accounts, including credit cards. Having a lower utilization rate is healthy for your credit scores.

Even though your overall credit utilization is what counts the most, utilization rates on individual accounts can also have a significant effect on your credit scores. Having many of your accounts with balances makes you a risky person for the lender. Therefore, pay close attention to your utilization on individual credit cards.

Please note that you can pay your owed amount in full every month and still appear to have a high overall utilization rate. This because your credit card issuers send reports to the bureaus at different times of the month. Therefore, make it a habit to make early payments if you want to maintain a low utilization rate.

Length of credit history

There are a variety of factors relating to the length of your credit history that can affect your score including the age of your newest account and oldest account, frequency of using your accounts, and the average age of your accounts.

Having many new accounts lowers the average age of your accounts, which in turn hurt your scores. Closed accounts could increase the average age of your accounts as they can stay on your credit reports for up to ten years. However, once they are erased, your score will be hurt. The impact could be felt more if the closed account was the oldest account.

New credit

While new accounts boost your FICO credit score, it doesn’t mean that opening multiple accounts almost at the same time will boost your credit score. In fact, creditors can interpret this to mean that you are looking for ways to access more credit.

New accounts lower your average account age, which ultimately affects your credit scores.

Credit mix

While this may somehow be vague, repaying a variety of debt indicates that you can handle different credits. Therefore, having a good mix of installment loans portray you as a more reliable person for lenders.

On the other hand, people with no credit are viewed as higher risk people than people who have managed different credit card responsibly.

If you focus on improving the above factors, you could improve your overall credit health.

Let’s now talk about why credit score matters before we can discuss how to improve it.

Why Your Credit Score Matters

You may ask, why should you endeavor to have a good credit score? And the simple to this that businesses and lenders will use check your credit score to make their decision regarding whether or not you are a reliable person to do business with and determine the rates you deserve.

Having a strong credit score can open up more opportunities for you. Here are a few ways good credit score can be beneficial to you;

Access to large-sized financing

If you are looking for large ticket loans from traditional financial institutions such as small business loan, mortgage, or auto loan, your first place to go is the bank. You may spend hours filling out paperwork and looking for guarantors, but one major thing that will determine whether or not you will qualify for a large-ticket rate and what rate your lender will offer is your credit score.

Therefore, if you know you will need a large loan soon, you will want to ensure that your credit score is healthy. A good score can help you qualify for a huge loan and help you get the best rates, which will ultimately help you save.

Qualify for a broader range of credit cards

Nowadays, it is easy to get a credit card, even if you have no credit history or poor credit, but you may have limited options. With a good credit score, you can access a variety of credit cards that reward new customers with sign up bonuses and points.

Therefore, it is important to start building a healthy credit history early on to avoid missing out on accessing popular credit cards or encountering limitations.

Best rates on a car loan

For most people, a car is the 2nd most important investment one can make after acquiring a home. With a great credit score, you can get the best rates on a car loan.

Therefore, if you are planning on buying a car soon, work on your credit score. This might help save you a significant amount in interest rates.

More options and better interest rates on online loans

Online lenders have become a popular alternative to traditional sources of finances. They deliver quicker loans and require simple securities- your credit score. Before approving a loan, they perform soft credit checks to see how much money to lend you. A strong credit score can help you get access to larger amounts and better interest rates from online lenders.

A healthy credit score can help you get access to affordable insurance premiums as insurance providers evaluate applicant’s probability to pay their insurance payment consistently and on time. An excellent credit score gives insurance providers confidence that you will meet your obligations.

Now that you understand what is a good credit score and why it matters, let’s wind up our guide by discussing how to improve your credit score and how you can achieve an excellent rating.

How to Fix a Poor Credit Score

Having a bad credit score may end up costing you hundreds or thousands of dollars and can make things difficult for you. The right way to fix your credit score is to do it yourself by paying your bills on time and cutting down outstanding debts. Sadly, most people fall for scams that promise to offer overnight credit repair.

If you have years of high credit card balances, an overdue student loan, or even a foreclosure, the chances are high that you have bad credit. The good news is that you can begin the critical journey to repairing your bad score. Here is how:

Figure out where you stand

Start by checking your annual reports, which is free through AnnualCreditReport.com. Note that there are deceptive websites that may claim to offer this service, but kindly stick to a credible source.

You need to check the reports carefully for any errors. Ensure you dispute any inaccurate or missing information by contacting your lender. The most likely mistakes that lead to poor credit score are late payments or too many inquiries.

Pay any credit balances

Do you have any outstanding credit balances? Pay them bit by bit each month until they are gone. Understand what your credit limit is, and make every effort to stay well under the maximum charging items.

Don’t apply for new credit

Most people with a poor credit rating may be faced with the temptation to open a new credit card. Kindly resist the temptation even when a store offers a discount on your purchase.

Each credit you apply for appears as a “hard inquiry” on your credit report, which means that if you have too many within two years, your credit score suffers more.

For you who has a below-average credit score, these inquiries may further delay your goal of watching your credit score rise.

Pay your taxes

If you haven’t cleared your taxes, the government may put a lien on your tax which reflects on your credit report. Unpaid tax liens can stay on your report indefinitely, but paid tax liens remain for seven years from the date of payment.

Fortunately, you can request a withdrawal after you have paid the taxes so that the notice of lien doesn’t appear on your credit report.

How Can You Achieve an Excellent Credit Score?

Well, credit scores range from 300 to 850. A score that falls anywhere between 700 and 750 is considered a good credit score, but it depends on the scoring method used. However, almost all lenders and financial companies use the FICO score. Now that you know what is considered a good credit score, here are five ways to achieve an excellent score:

Check your score regularly

Checking your score helps you see if you are making the right strides to improving your score. You learn what is hurting your credit score so that you can minimize the mistakes.

Avoid spending more than you can afford

Once you deal with mistakes and errors on your credit score, ensure that you spend according to your means. Why is this important? It helps you pay bills on time, pay down debt, and avoid applying for credit. The only way to achieve these three things is to have a budget.

To begin, review your tax returns for the past two years to get a picture of how much money you earn every year. Next, estimate your monthly spending habits and create a limit based on your income.

Pay all bills on time

To avoid having bad credit, keep your monthly bills on time. That is all you need. On-time payments are an important factor in achieving an excellent credit score.

Apply for new credit only as needed

Opening new credit accounts to have a better credit mix won’t likely improve your credit score. As said earlier, having too many credits can harm your score in numerous ways; from putting too many hard inquiries on your reports to tempting you to spend more. Refrain from applying for several credit cards within a short time frame or when applying for a large loan.

Be patient

Raising your credit score will take time. Therefore, the best way to achieve an excellent score is by developing good long-term habits. Establish the right practices like keeping a low utilization rate, paying debts on time, and this should reflect on your credit score over time.

Bottom Line

Establishing a solid credit score can help you unlock more opportunities, especially in terms of financial access. Your credit score offers an easy way for businesses and lenders to judge whether or not to work with you. It also influences the interest rates you pay for your loans. To set yourself up for success in the future, and gain access to savings, opportunities, and credit your deserve, start investing in your credit health. We hope that our guide has opened up your eyes about what is a good credit score, how credit scores are calculated, why it matters, and how you can improve it. With this knowledge, you will find it easy to improve and maintain your credit score.